Taxation of Foreign Dividends in the Hands of South African Residents Receiving Dividends from a Mauritius Discretionary Trust

Overview

The South African Budget Speech 2025/26, delivered by Finance Minister Mr. Enoch Godongwana on March 12, 2025, did not introduce any changes to the taxation of foreign dividends. The existing rules continue to apply, including a maximum effective tax rate of 20% on foreign dividends received by South African tax resident individuals from a foreign company.

This article explores the key taxation concepts applicable to South African tax resident individuals who are beneficiaries of a Mauritius discretionary trust holding shares in a Global Business Company (GBC) or an Authorised Company (AC).

What is a Foreign Dividend?

Understanding Foreign Dividends: Legal Definition and Implications

A foreign dividend, as defined in section 1(1) of the South African Income Tax Act (“the Act”), refers to any amount paid or payable by a foreign company in respect of its shares, provided it is treated as a dividend under the tax laws of the company’s jurisdiction.

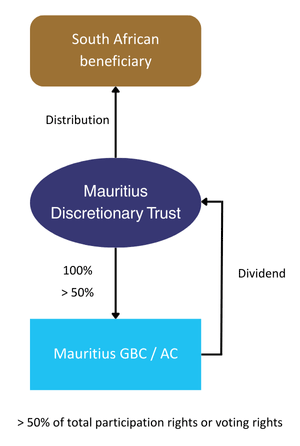

When a Mauritius GBC or AC distributes dividends to a Mauritius discretionary trust, which then makes a distribution to a South African beneficiary, it falls within this definition.

The definition of foreign dividend further stipulates that in order for an amount to qualify as a foreign dividend, it must be treated as a dividend or similar payment by that foreign company for purposes of the laws relating to tax on income on companies of the country in which that foreign company has its place of effective management.

For a structure to be tax-efficient, proper planning is crucial. Simply establishing a foreign trust and foreign company such as a Mauritius trust and a GBC / AC, without strategic foresight and expert structuring, could lead to unintended tax consequences in South Africa and potentially in the foreign jurisdiction as well!

Tax Treatment of Foreign Dividends in South Africa

Dividends Tax Considerations

Foreign dividends are not subject to South African dividends tax unless paid on listed shares on the Johannesburg Stock Exchange (JSE) and do not constitute an in-specie asset distribution.

Since dividends paid by a Mauritius GBC or AC to a Mauritius discretionary trust do not fall under these conditions, they are not subject to South African dividends tax.

Normal Taxation of Foreign Dividends in South Africa

Foreign dividends form part of “gross income” under the Act and are subject to normal tax unless they qualify for exemptions under Section 10B.

Tax Exemptions for Foreign Dividends

- Full exemption (Participation Exemption):

- Applies if the recipient directly holds at least 10% of the equity shares and voting rights in the foreign company paying the dividend.

- Indirect shareholding through a trust does not qualify.

- Partial exemption:

- If the participation exemption does not apply, 25/45 of the foreign dividend received by natural persons, deceased estates, insolvent estates, and trusts may be exempt from tax.

- This effectively subjects the remaining portion to a maximum 20% tax rate.

Attribution Rules: Sections 7(8)(aA) & 25B(2B)

Section 7(8)(aA): Attribution of Foreign Trust Income

Effective from March 1, 2019, this provision applies when:

- A South African resident funds a foreign trust via an interest-free or low-interest loan, donation, or settlement.

- The foreign trust holds more than 50% of the shares in a foreign company.

If applicable, the participation exemption is ignored when calculating the tax liability of a South African beneficiary.

A typical structure in Mauritius would be:

Practical Example of Attribution

A South African resident makes an interest-free loan of USD 10,000 to a Mauritius trust, which then acquires 100% of a GBC’s shares. The GBC generates income and distributes USD 2,000 as dividends to the trust, which in turn distributes USD 1,000 to the South African beneficiary in the same fiscal year. If the beneficiary is taxed at 45%, the tax payable would be:

20/45 X USD 1,000 = USD 444

USD 444 x 45% = ~ USD 200

This results in an effective tax rate of 20%. Since the loan was interest-free, the full amount is deemed to be a donation, disposition, or settlement.

Section 25B(2B): Taxation of Accumulated Dividends

This rule applies when a foreign dividend is accumulated in a trust and distributed to a South African beneficiary in a later tax year. In such cases, the full participation exemption is disregarded, but the partial exemption (25/45) may still apply.

If the dividend is distributed within the same tax year in which it accrues to the trust, Section 25B(2B) does not apply.

Where a South African resident is a beneficiary of a Mauritius discretionary trust which holds at least 10% but less than 50% of the foreign company, the full participation exemption shall still not be available to him as he does not directly hold the shares in the Mauritius GBC. The partial exemption may however still be available.

Foreign Tax Rebate in South Africa

Under Section 6quat, a South African tax resident may claim a foreign tax rebate if foreign withholding tax was levied on dividends before distribution to the trust. This helps mitigate double taxation, but the rebate is limited to the South African tax payable on the dividend.

Mauritius Taxation Considerations

- Dividends paid by a Mauritius GBC or AC are exempt from Mauritius corporate tax and withholding tax.

- A Mauritius trust, if structured as a non-resident trust, is not subject to Mauritius corporate tax on its foreign income.

- Any distribution by a Mauritius trust to a beneficiary is treated as a dividend and is not subject to withholding tax in Mauritius.

Compliance with International Tax Norms

Mauritius has implemented substantial tax reforms to align with OECD international standards. The France based OECD Forum on Harmful Tax Practices (FHTP) has confirmed that Mauritius does not have harmful tax practices, making it a globally recognized and compliant jurisdiction.

To fully benefit from Mauritius’ tax advantages, compliance with the reformed tax framework is essential.

There is no substitute for expert guidance and expertise when venturing into the international arena of global business structuring and international taxation!

Conclusion

For South African tax residents who are beneficiaries of a Mauritius discretionary trust, understanding the tax implications of foreign dividends is crucial. While a well-structured Mauritius GBC/AC & trust arrangement can optimize tax efficiency, distributions to South African beneficiaries remain taxable, at least partially.

Given the complexity of cross-border taxation and South Africa’s stringent compliance landscape, expert advice is critical.

At GWMS Ltd, we specialize in designing tax-efficient international structures that align with regulatory requirements while optimizing benefits for our clients.

Contact us today to explore how we can assist you in optimizing your international tax structure.

Leave a Reply

Want to join the discussion?Feel free to contribute!